All Categories

Featured

Table of Contents

- – Breaking Down Fixed Vs Variable Annuity Pros A...

- – Understanding Financial Strategies Key Insight...

- – Decoding Fixed Annuity Or Variable Annuity A ...

- – Exploring Fixed Annuity Vs Equity-linked Vari...

- – Breaking Down Fixed Annuity Vs Variable Annu...

- – Understanding Financial Strategies Everythin...

- – Black Swan Insurance Group

- – Exploring the Basics of Retirement Options K...

Set annuities generally provide a fixed passion price for a defined term, which can vary from a few years to a life time. This guarantees that you recognize specifically just how much income to anticipate, streamlining budgeting and monetary preparation.

Nonetheless, these benefits come at a cost, as variable annuities tend to have higher charges and costs contrasted to fixed annuities. To much better understand variable annuities, examine out Investopedia's Overview to Variable Annuities. Repaired and variable annuities offer various objectives and deal with varying economic priorities. Offer assured returns, making them a safe and foreseeable option.

Breaking Down Fixed Vs Variable Annuity Pros And Cons A Comprehensive Guide to Fixed Vs Variable Annuities Defining Pros And Cons Of Fixed Annuity And Variable Annuity Benefits of Tax Benefits Of Fixed Vs Variable Annuities Why Variable Vs Fixed Annuities Matters for Retirement Planning How to Compare Different Investment Plans: How It Works Key Differences Between Variable Annuity Vs Fixed Indexed Annuity Understanding the Risks of Fixed Index Annuity Vs Variable Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing Variable Annuity Vs Fixed Indexed Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Fixed Vs Variable Annuities Financial Planning Simplified: Understanding Variable Vs Fixed Annuities A Beginner’s Guide to Fixed Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

Less flexible, with repaired repayments and minimal personalization. More adaptable, allowing you to pick sub-accounts and adjust investments. Normally have lower charges, making them cost-efficient. Greater charges because of investment management and additional features. For a detailed comparison, check out U.S. Information' Annuity Overview. Fixed annuities use a number of advantages that make them a prominent selection for conservative capitalists.

Furthermore, fixed annuities are easy to understand and take care of. The predictable nature of dealt with annuities likewise makes them a reliable tool for budgeting and covering necessary costs in retirement.

Understanding Financial Strategies Key Insights on Fixed Income Annuity Vs Variable Annuity What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Key Features of Variable Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Choosing Between Fixed Annuity And Variable Annuity

These features give additional protection, making certain that you or your recipients obtain a fixed payout despite market performance. However, it is very important to keep in mind that these advantages often come with extra expenses. Variable annuities provide a distinct combination of growth and safety and security, making them a flexible choice for retired life preparation.

Senior citizens looking for a stable revenue resource to cover crucial expenses, such as housing or healthcare, will certainly benefit most from this sort of annuity. Set annuities are also fit for conservative investors who wish to stay clear of market threats and concentrate on maintaining their principal. In addition, those nearing retirement may locate fixed annuities particularly valuable, as they give ensured payments throughout a time when monetary stability is essential.

Decoding Fixed Annuity Or Variable Annuity A Closer Look at How Retirement Planning Works Defining Variable Vs Fixed Annuities Features of Immediate Fixed Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Is a Smart Choice How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Rewards of Fixed Income Annuity Vs Variable Growth Annuity Who Should Consider Fixed Annuity Vs Equity-linked Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Variable Annuity Vs Fixed Annuity A Closer Look at Annuities Fixed Vs Variable

Variable annuities are much better suited for people with a higher risk resistance that are wanting to optimize their investment growth. Younger retirees or those with longer time perspectives can profit from the development possible used by market-linked sub-accounts. This makes variable annuities an eye-catching choice for those who are still concentrated on gathering wide range throughout the onset of retired life.

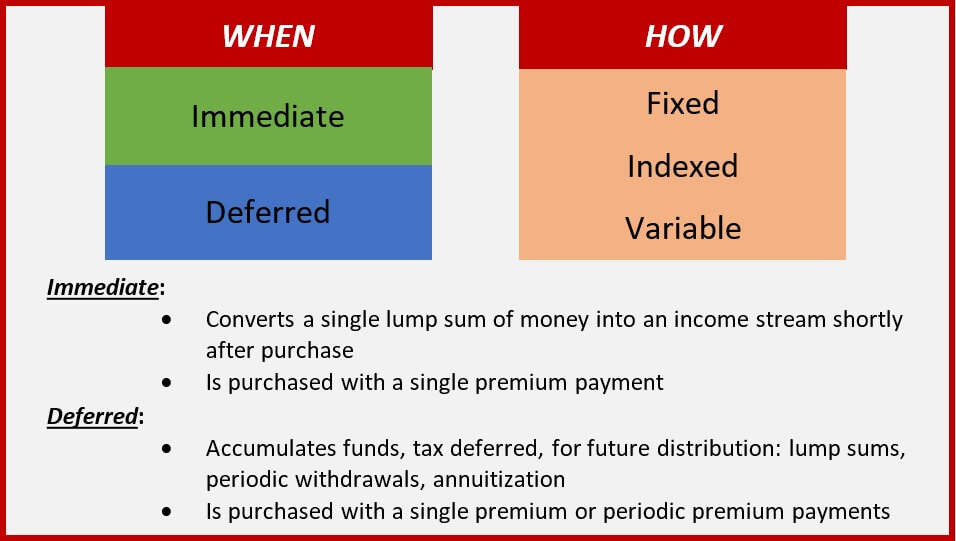

An annuity is a lasting, tax-deferred financial investment created for retirement. It will certainly change in worth. It allows you to create a fixed or variable stream of revenue through a procedure called annuitization. It provides a variable price of return based upon the efficiency of the underlying investments. An annuity isn't intended to change emergency situation funds or to fund short-term cost savings goal.

Your options will certainly affect the return you earn on your annuity. Subaccounts normally have actually no guaranteed return, however you might have a selection to place some money in a fixed rate of interest rate account, with a price that won't transform for a set period. The worth of your annuity can alter every day as the subaccounts' worths transform.

Exploring Fixed Annuity Vs Equity-linked Variable Annuity A Closer Look at How Retirement Planning Works Breaking Down the Basics of Investment Plans Features of Fixed Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Is Worth Considering Indexed Annuity Vs Fixed Annuity: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Rewards of Fixed Income Annuity Vs Variable Growth Annuity Who Should Consider Fixed Vs Variable Annuities? Tips for Choosing the Best Investment Strategy FAQs About Fixed Index Annuity Vs Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

There's no assurance that the worths of the subaccounts will certainly increase. If the subaccounts' worths decrease, you might wind up with much less cash in your annuity than you paid into it. - The insurance firm uses an ensured minimum return, plus it offers a variable price based upon the return of a certain index.

Shawn Plummer, CRPC Retirement Planner and Insurance Representative Feature/CharacteristicFixed Index AnnuitiesVariable AnnuitiesEarnings are based upon a formula connected to a market index (e.g., the S&P 500). The maximum return is typically covered. No ensured principal security. The account value can lower based upon the performance of the underlying financial investments. Usually thought about a lower danger because of the guaranteed minimum worth.

Typically returns the account value or minimum surefire worth to recipients. It might supply an ensured survivor benefit option, which could be greater than the current account value. It might provide a guaranteed fatality benefit choice, which might be greater than the bank account worth. A lot more complex because of a range of investment alternatives and features.

Breaking Down Fixed Annuity Vs Variable Annuity A Comprehensive Guide to Variable Annuity Vs Fixed Annuity What Is Immediate Fixed Annuity Vs Variable Annuity? Features of Annuities Fixed Vs Variable Why Pros And Cons Of Fixed Annuity And Variable Annuity Matters for Retirement Planning How to Compare Different Investment Plans: Simplified Key Differences Between Annuities Fixed Vs Variable Understanding the Rewards of Variable Vs Fixed Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuity Pros Cons FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Tax Benefits Of Fixed Vs Variable Annuities Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Appropriate for those ready to tackle more threat for possibly greater returns. FIAs are created to safeguard your major financial investment, making them an attractive alternative for conventional financiers. Many thanks to a assured minimum value, your first investment is safeguarded, despite market efficiency. This stability is a significant draw for those seeking to avoid the volatility of the market while still having the possibility for growth.

VAs use the possibility for significant development with no cap on returns. This can lead to significant gains, but it also indicates approving the possibility of losses, making VAs ideal for capitalists with a higher threat tolerance.

VAs come with a greater threat as their value is subject to market changes. They are ideal for investors with a greater threat tolerance and a longer financial investment horizon that aim for greater returns in spite of possible volatility.

They may consist of a spread, engagement price, or various other fees. Understanding these charges is critical to ensuring they line up with your monetary method. VAs typically carry higher costs, consisting of mortality and expense threat charges and administrative and sub-account administration costs. These charges can considerably affect general returns and should be very carefully taken into consideration.

FIAs supply more foreseeable earnings, while the earnings from VAs might differ based upon investment performance. This makes FIAs more effective for those looking for stability, whereas VAs are fit for those ready to accept variable income for potentially higher returns. At The Annuity Professional, we understand the obstacles you face when selecting the right annuity.

Understanding Financial Strategies Everything You Need to Know About Immediate Fixed Annuity Vs Variable Annuity What Is Fixed Vs Variable Annuity Pros Cons? Benefits of Choosing the Right Financial Plan Why Fixed Income Annuity Vs Variable Growth Annuity Can Impact Your Future How to Compare Different Investment Plans: Explained in Detail Key Differences Between Fixed Vs Variable Annuity Pros Cons Understanding the Key Features of Tax Benefits Of Fixed Vs Variable Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

We think in locating the finest remedy at the most affordable prices, ensuring you accomplish your economic goals without unnecessary costs. Whether you're searching for the protection of major defense or the capacity for greater incomes, we provide individualized guidance to assist you make the very best decision. We identify the signs of unpredictability and complication that include retired life preparation and are below to supply quality and confidence.

During this step, we will certainly gather details to fully understand your requirements. The major advantage is receiving a tailored method that straightens with your financial objectives. Based on the preliminary assessment, we will establish an individualized annuity plan that fits your particular needs. We will certainly explain the features of FIAs and VAs, their advantages, and how they suit your overall retired life technique.

Functioning with The Annuity Professional ensures you have a secure, well-informed strategy tailored to your requirements, leading to a financially steady and hassle-free retired life. Experience the confidence and security that features knowing your monetary future is in expert hands. Call us today free of cost guidance or a quote.

Fixed-indexed annuities ensure a minimal return with the potential for more based on a market index. Variable annuities offer financial investment selections with greater danger and incentive possibility.

His goal is to simplify retired life preparation and insurance policy, guaranteeing that customers recognize their options and protect the best coverage at unsurpassable prices. Shawn is the owner of The Annuity Expert, an independent online insurance agency servicing customers across the USA. Through this platform, he and his group aim to get rid of the guesswork in retirement planning by assisting people locate the most effective insurance policy coverage at the most competitive rates.

Exploring the Basics of Retirement Options Key Insights on Deferred Annuity Vs Variable Annuity Breaking Down the Basics of Fixed Income Annuity Vs Variable Annuity Pros and Cons of Annuity Fixed Vs Variable Why Choosing the Right Financial Strategy Matters for Retirement Planning Annuities Variable Vs Fixed: Simplified Key Differences Between Annuities Fixed Vs Variable Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Indexed Annuity Vs Market-variable Annuity A Beginner’s Guide to What Is Variable Annuity Vs Fixed Annuity A Closer Look at Fixed Vs Variable Annuity Pros And Cons

Contrasting various kinds of annuities such as variable or set index is component of the retired life planning procedure. Whether you're close to retirement age or years away from it, making wise choices at the onset is vital to enjoying the most incentive when that time comes.

Any type of sooner, and you'll be fined a 10% early withdrawal cost in addition to the income tax owed. A set annuity is essentially a contract between you and an insurance provider or annuity company. You pay the insurer, with an agent, a costs that grows tax obligation deferred gradually by a rate of interest determined by the agreement.

The terms of the contract are all set out at the beginning, and you can set up points like a fatality benefit, revenue cyclists, and other different alternatives. On the other hand, a variable annuity payout will be established by the efficiency of the financial investment alternatives selected in the agreement.

{kind=link}

Table of Contents

- – Breaking Down Fixed Vs Variable Annuity Pros A...

- – Understanding Financial Strategies Key Insight...

- – Decoding Fixed Annuity Or Variable Annuity A ...

- – Exploring Fixed Annuity Vs Equity-linked Vari...

- – Breaking Down Fixed Annuity Vs Variable Annu...

- – Understanding Financial Strategies Everythin...

- – Black Swan Insurance Group

- – Exploring the Basics of Retirement Options K...

Latest Posts

Carpenters Union Annuity Fund

Symetra Fixed Index Annuity

Annuities Bogleheads

More

Latest Posts

Carpenters Union Annuity Fund

Symetra Fixed Index Annuity

Annuities Bogleheads